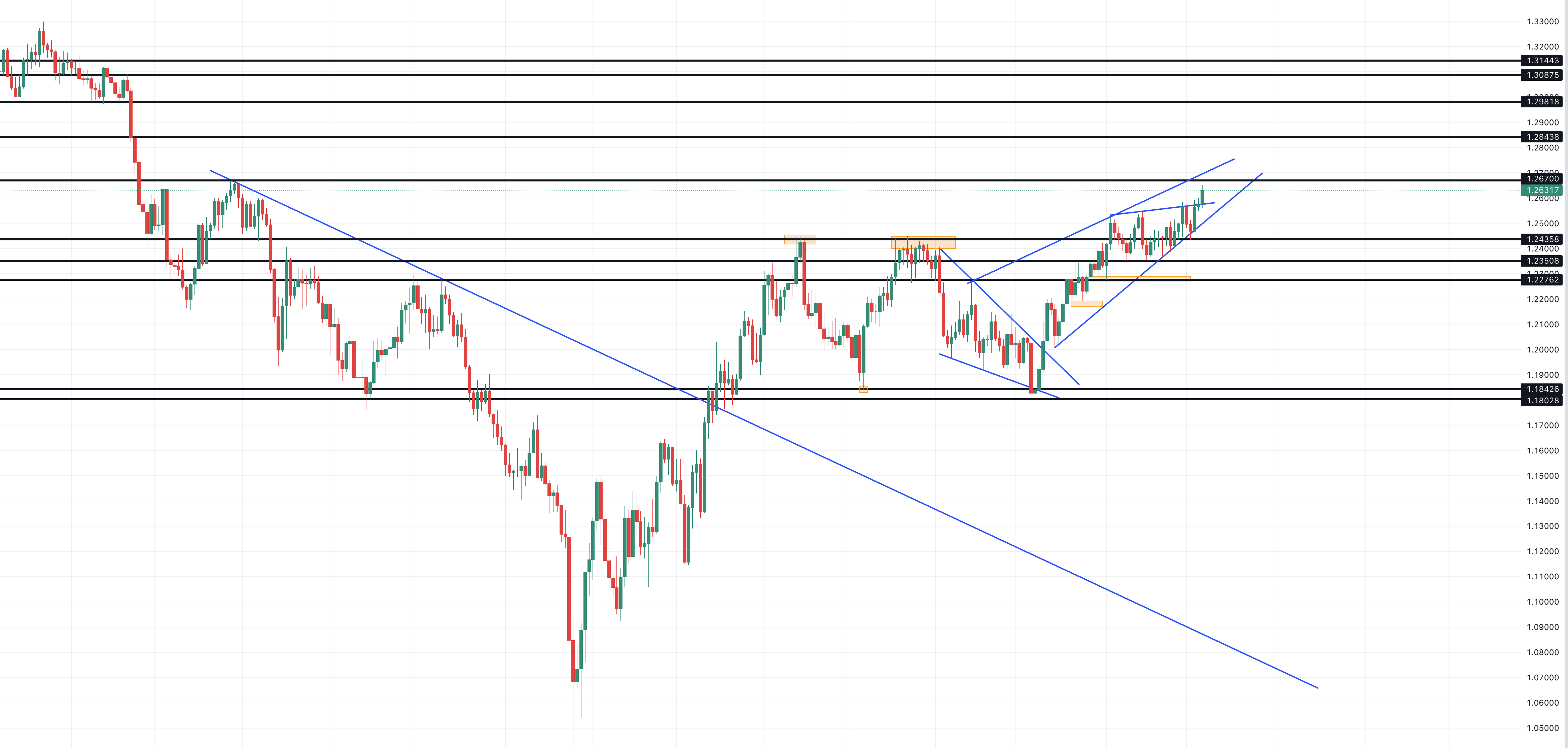

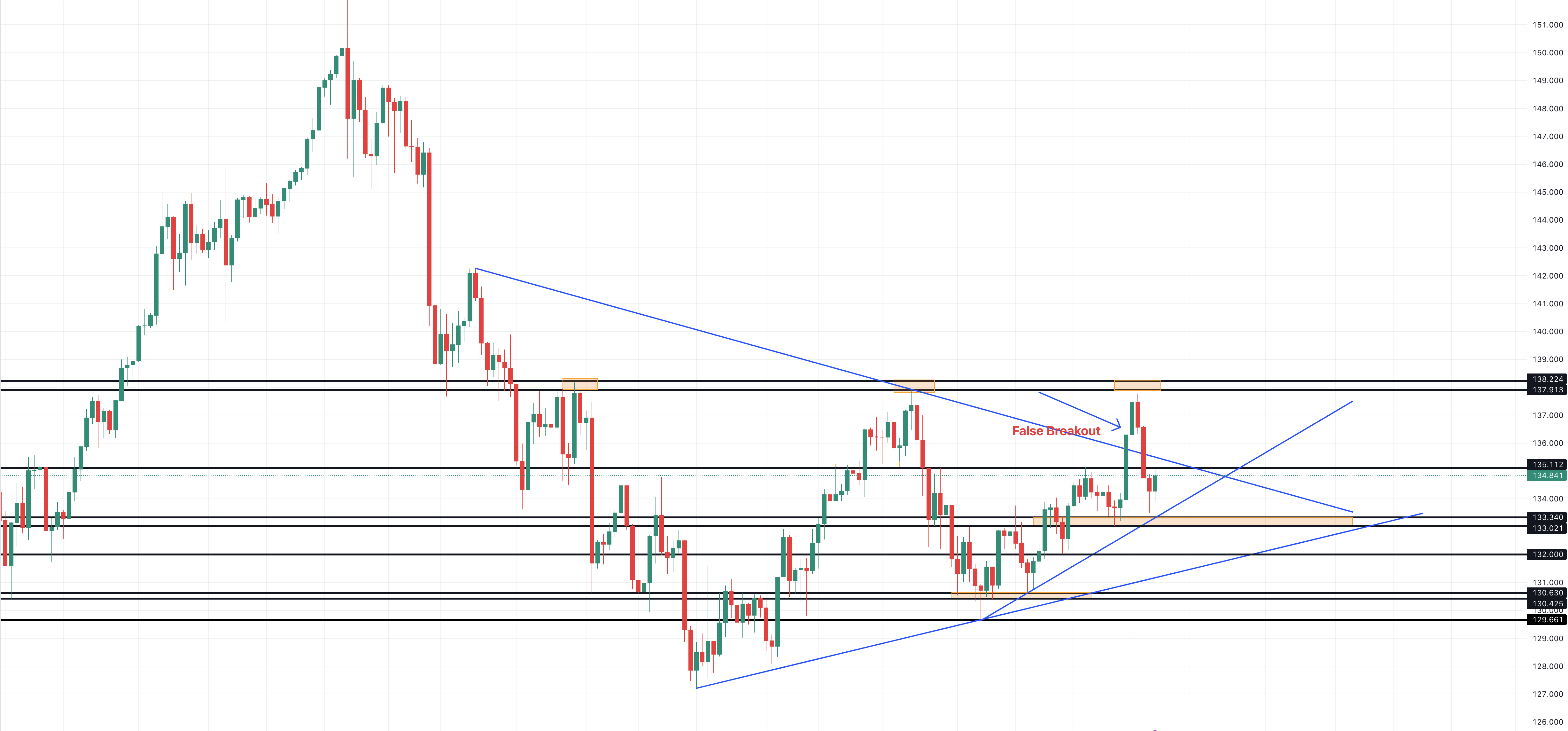

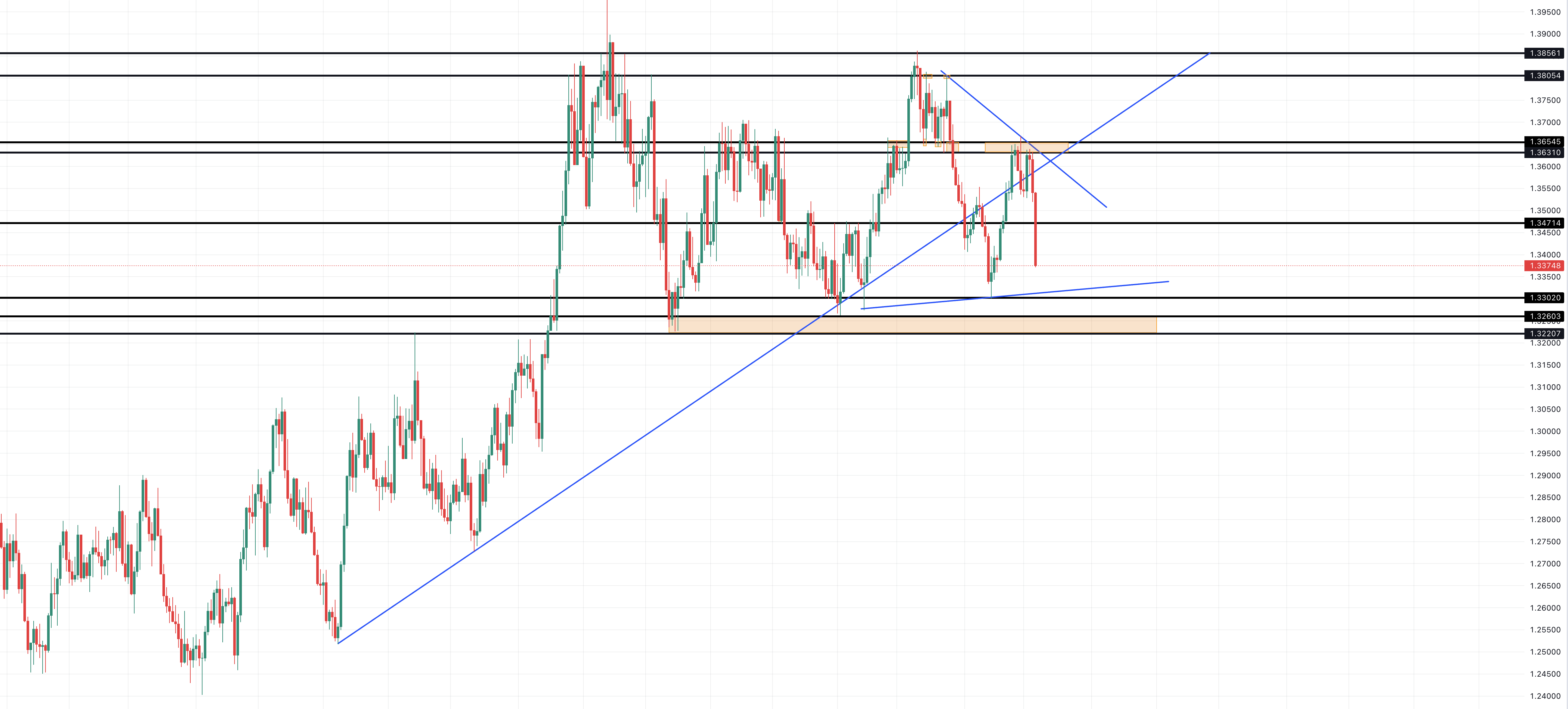

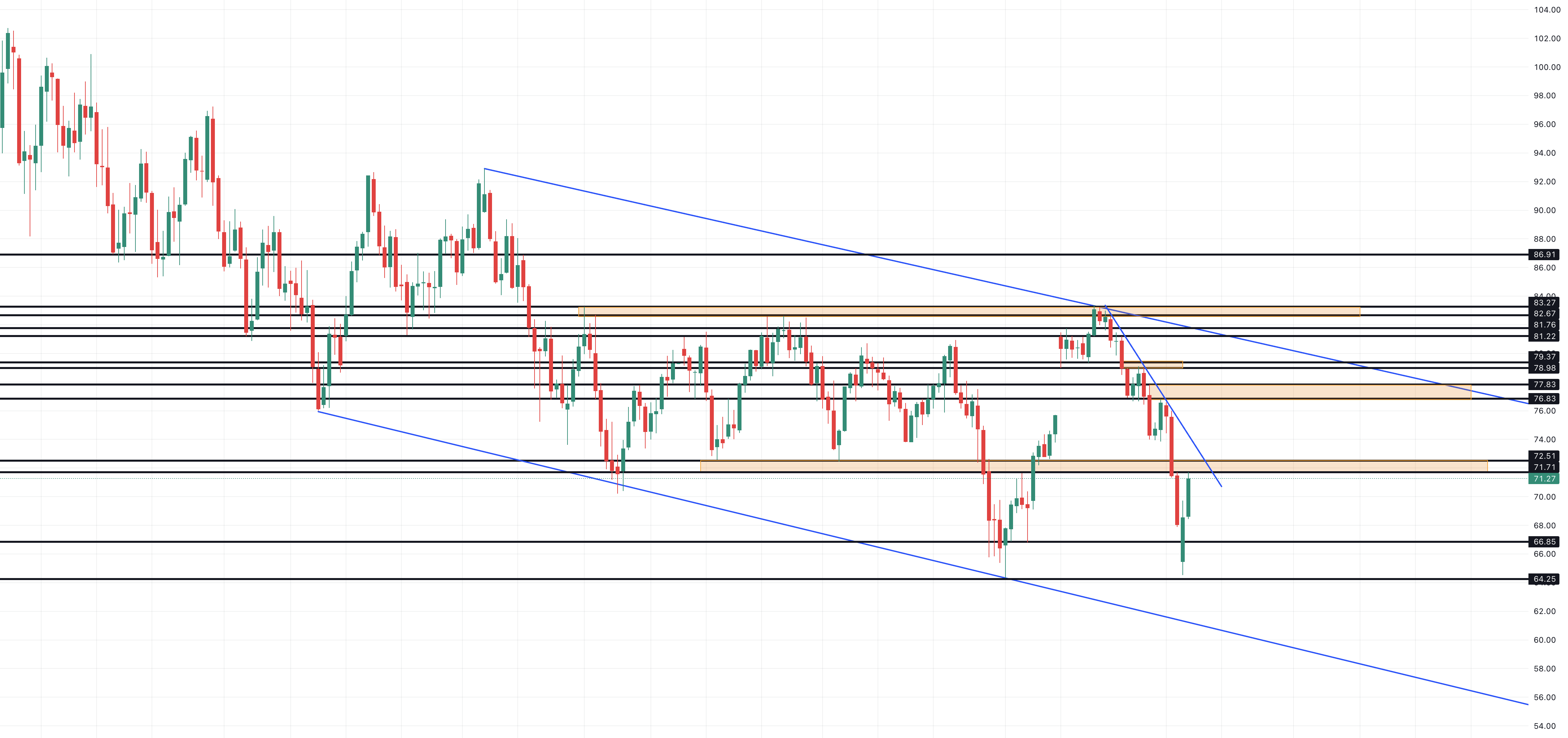

During this month, investors remain uncertain about the future of the monetary policy in the US after the FED decided to raise interest rates by 25bps as widely expected, hinting at a pause in the rate-hiking campaign and closing the door for a potential rate cut in the near term.

However, Chairman Powell announced that the FED’s future policy will likely be data-dependent, and inflation will continue to be monitored actively.

Meanwhile, we have seen a strong employment report in April as the Non-Farm payrolls rose to 253K compared to expectations of only 181K, in addition, the average hourly earnings increased from 0.3% to 0.5% while the unemployment rate fell from 3.5% to 3.4%.

For now, all eyes will be on the upcoming inflation data as the latest CPI is expected to have risen from 0.1% to 0.4% which can push the FED to extend its monetary policy tightening.

From a wider angle, the US banking crisis continues to weigh on investor sentiment following new bank failures which can keep stocks under pressure in the short term, on the opposite, a strong earnings report can help the market recover some early losses.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}