April is likely to be an interesting month as we kick off the second quarter of the year.

The FED raised interest rates by 25bps only in March, which shows that the US central bank is clearly slowing down the rate hike pace, which can lead to a potential pause in the current monetary policy tightening cycle. The FED goal remains clear, lowering inflation, however, reaching a soft landing is not an easy task amid an unstable economic environment.

The recent crisis in the banking sector is also weighing on FED’s future decisions. For those reasons, the US Dollar is expected to remain under pressure during this month.

Meanwhile, the labor market might face some weakness in April, the NFP forecasts are pointing to a lower reading. Analysts are seeing the US economy adding only 238K new jobs in March compared to 310K registered previously. On the other side, the unemployment rate is likely to remain unchanged at 3.6%.

The FED will continue to monitor inflation levels through the CPI figures and the latest developments in the labor market.

Consequently, there are high chances for gold to continue to shine as investors can look for asset rotation to hedge their risk exposure, and historically, the yellow metal remains an important safe haven during difficult times.

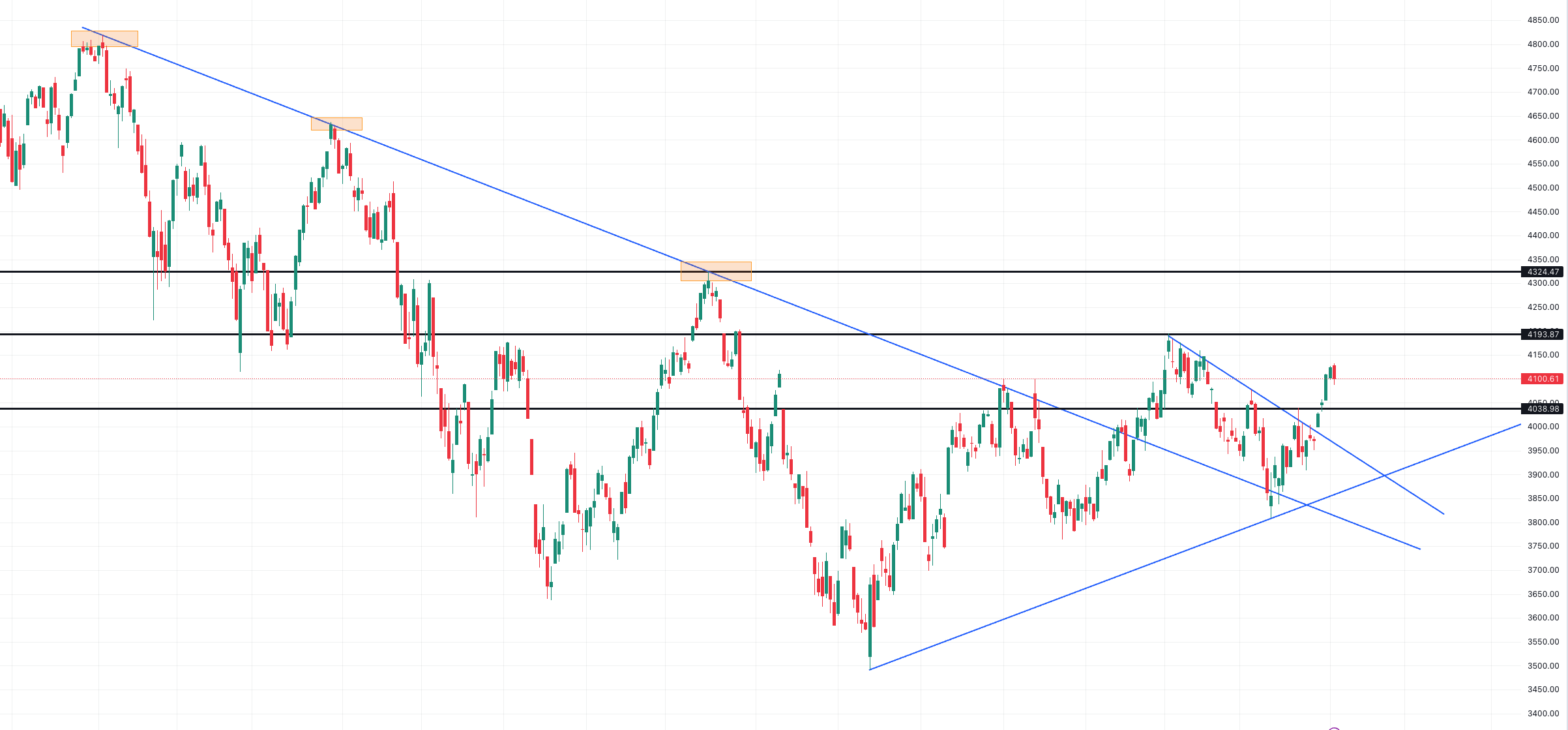

On the other side, following a short-term recovery, the US stock market might stabilize until we see how the FED will react to upcoming economic data.

Finally, Oil prices are expected to rise in April and challenge the $83 per barrel after reports that large oil producers with the OPEC+ group agreed to lower production by more than 1M barrels per day, starting at the beginning of next month and lasting toward the end of this year.

The decision of cutting production can create a strong imbalance between supply and demand levels and fundamentally, oil prices are expected to remain steady.

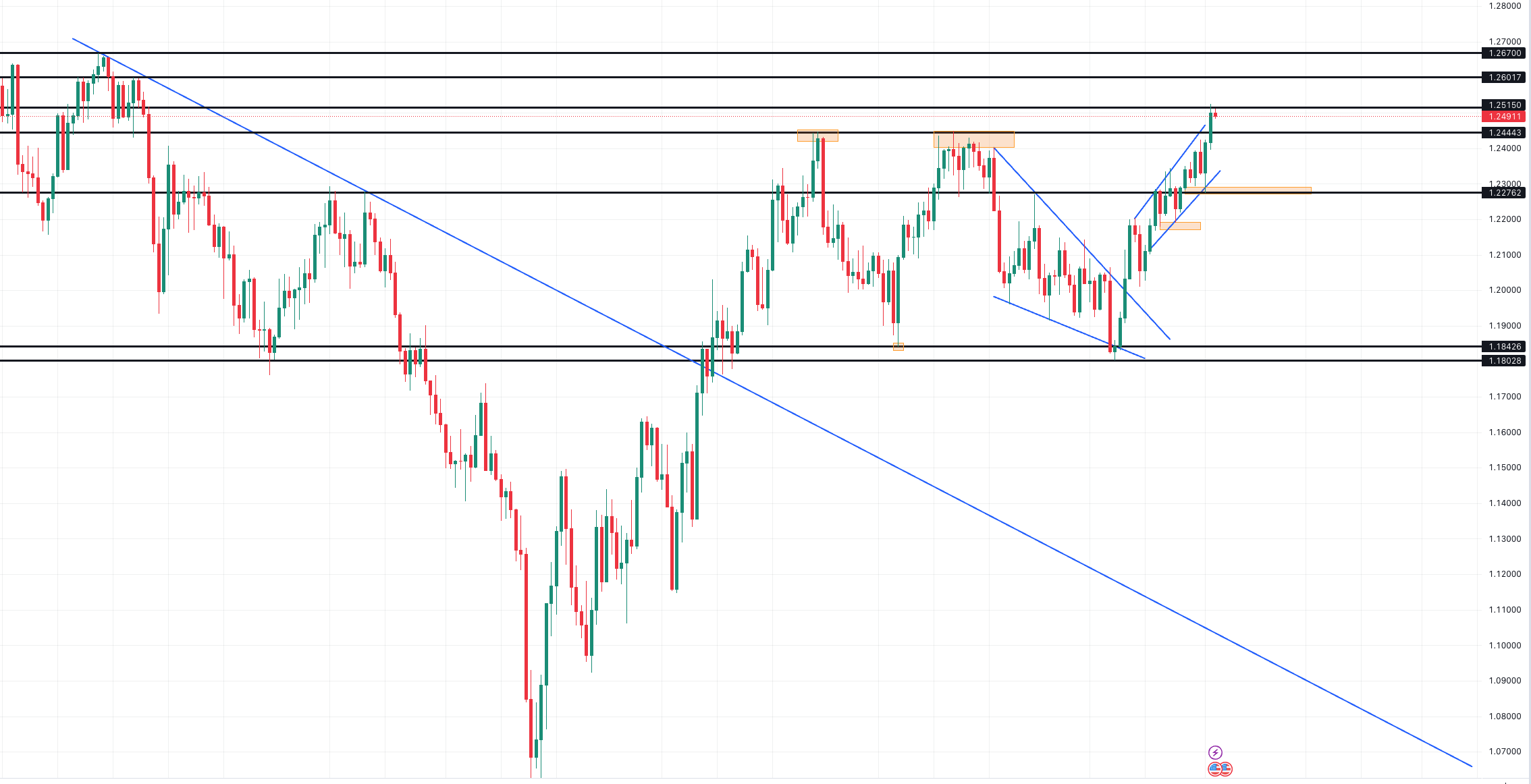

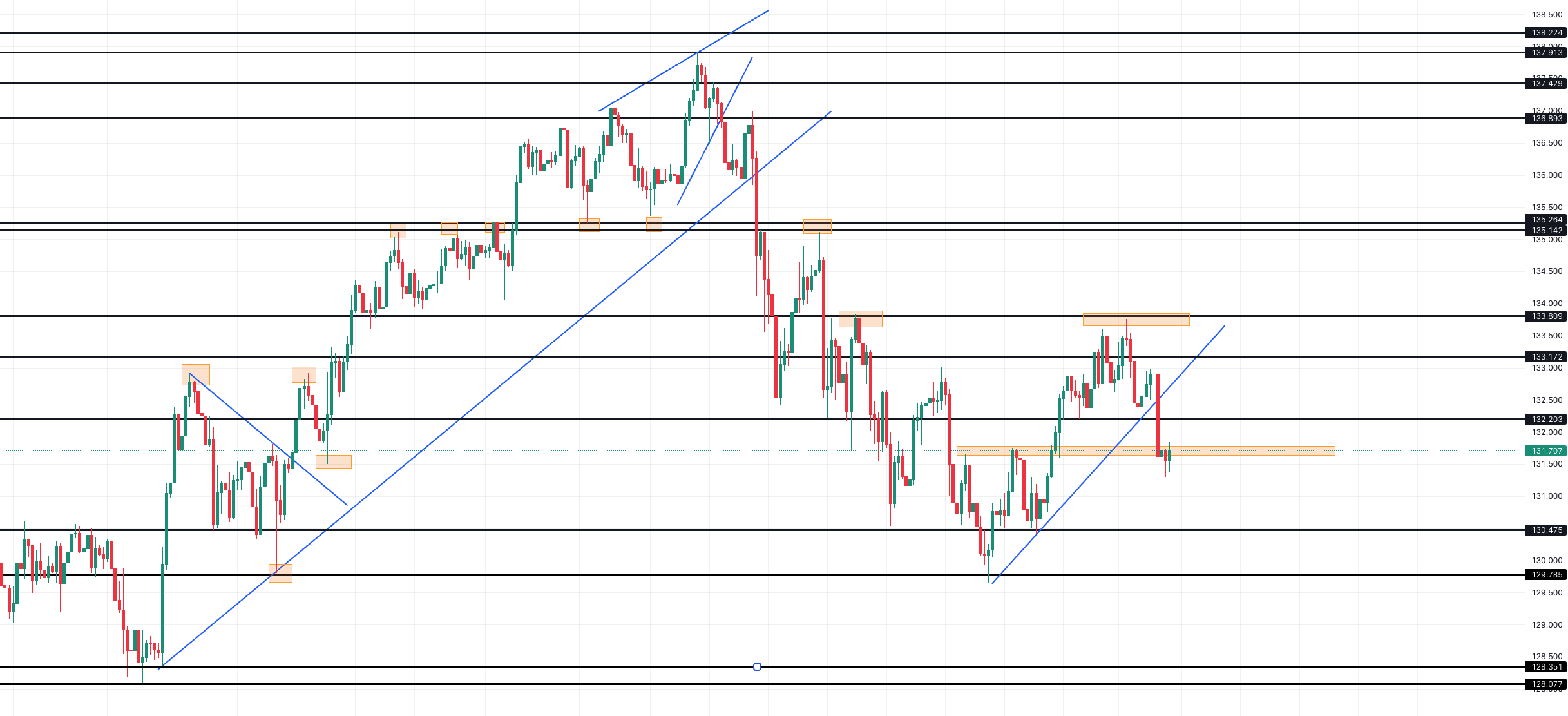

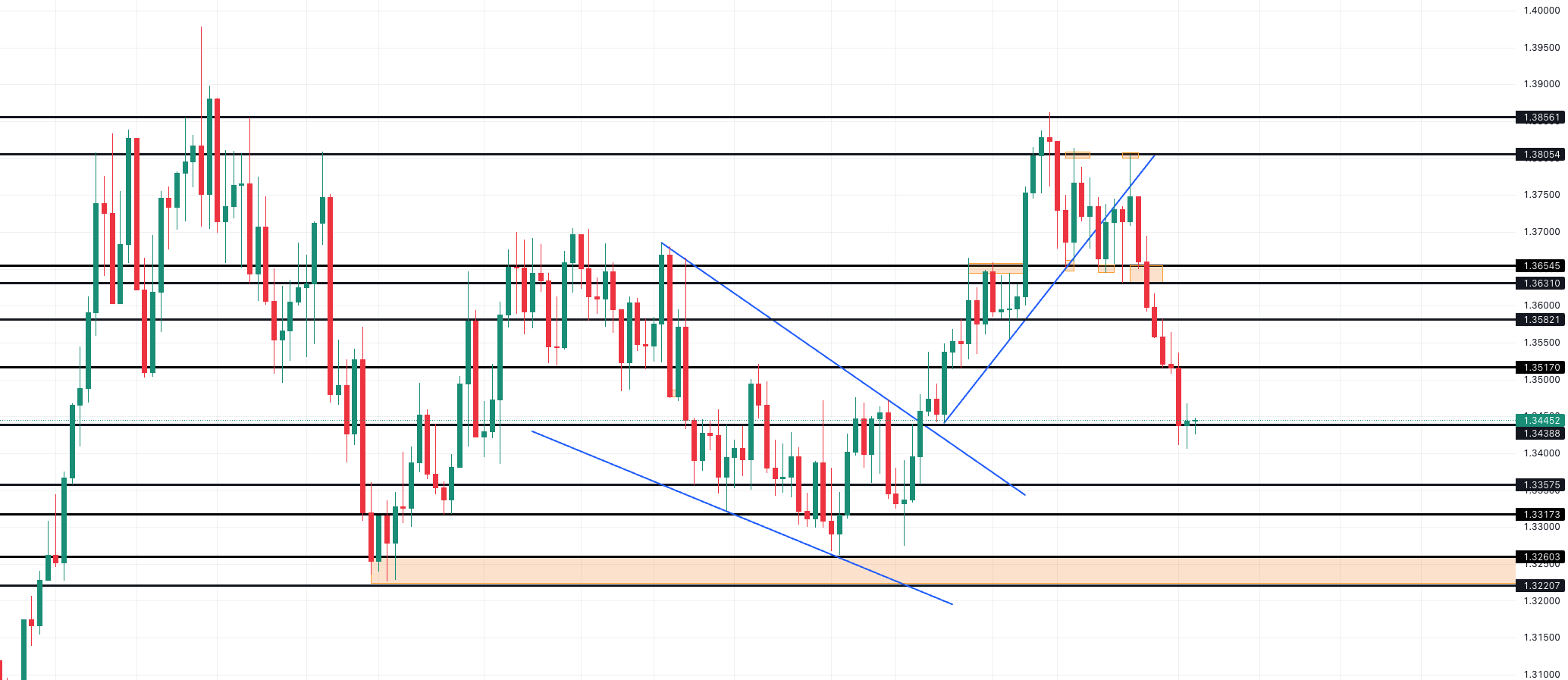

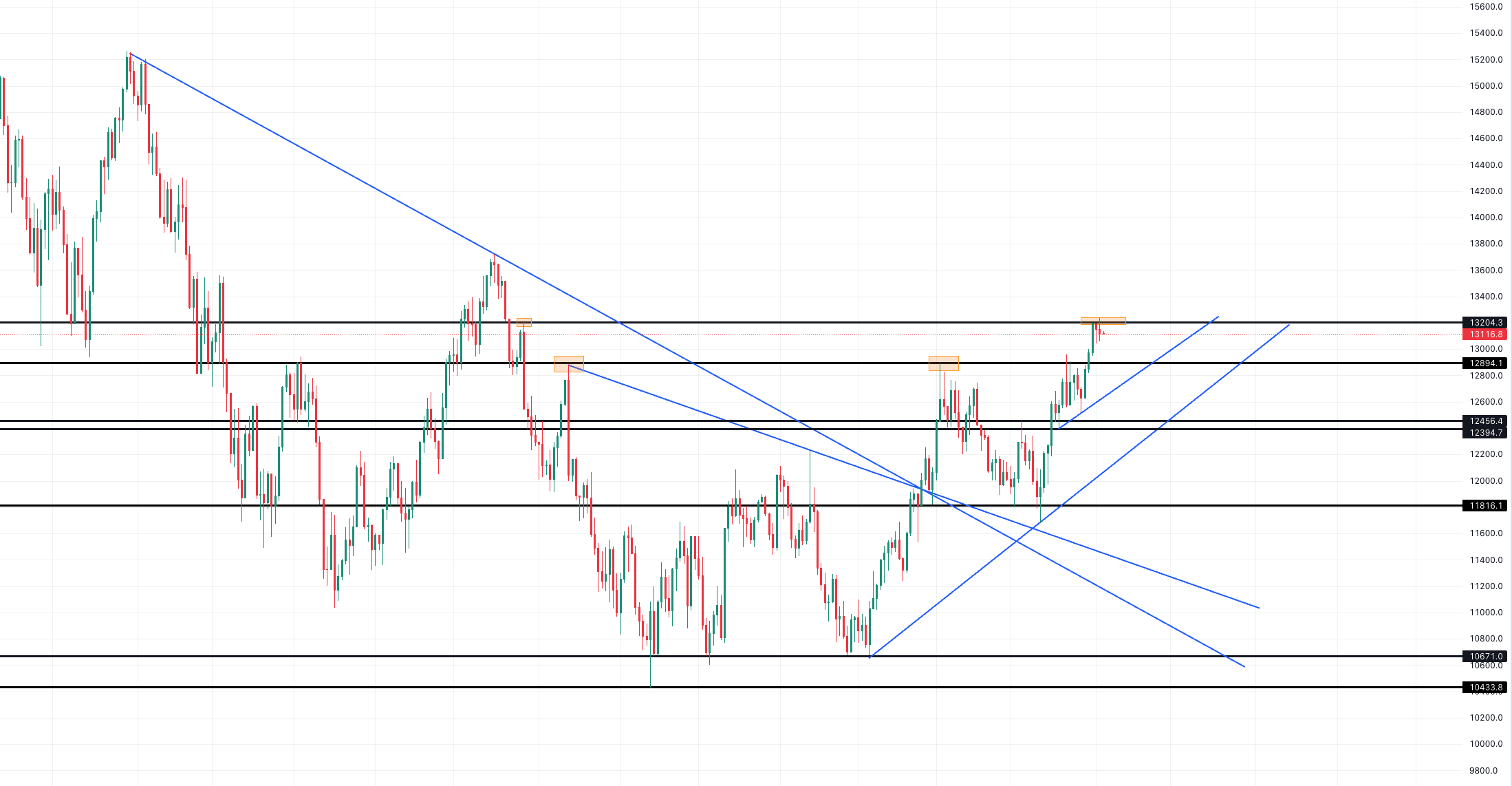

Now let us have a look at the monthly technical outlook for major currencies, commodities, and indices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}