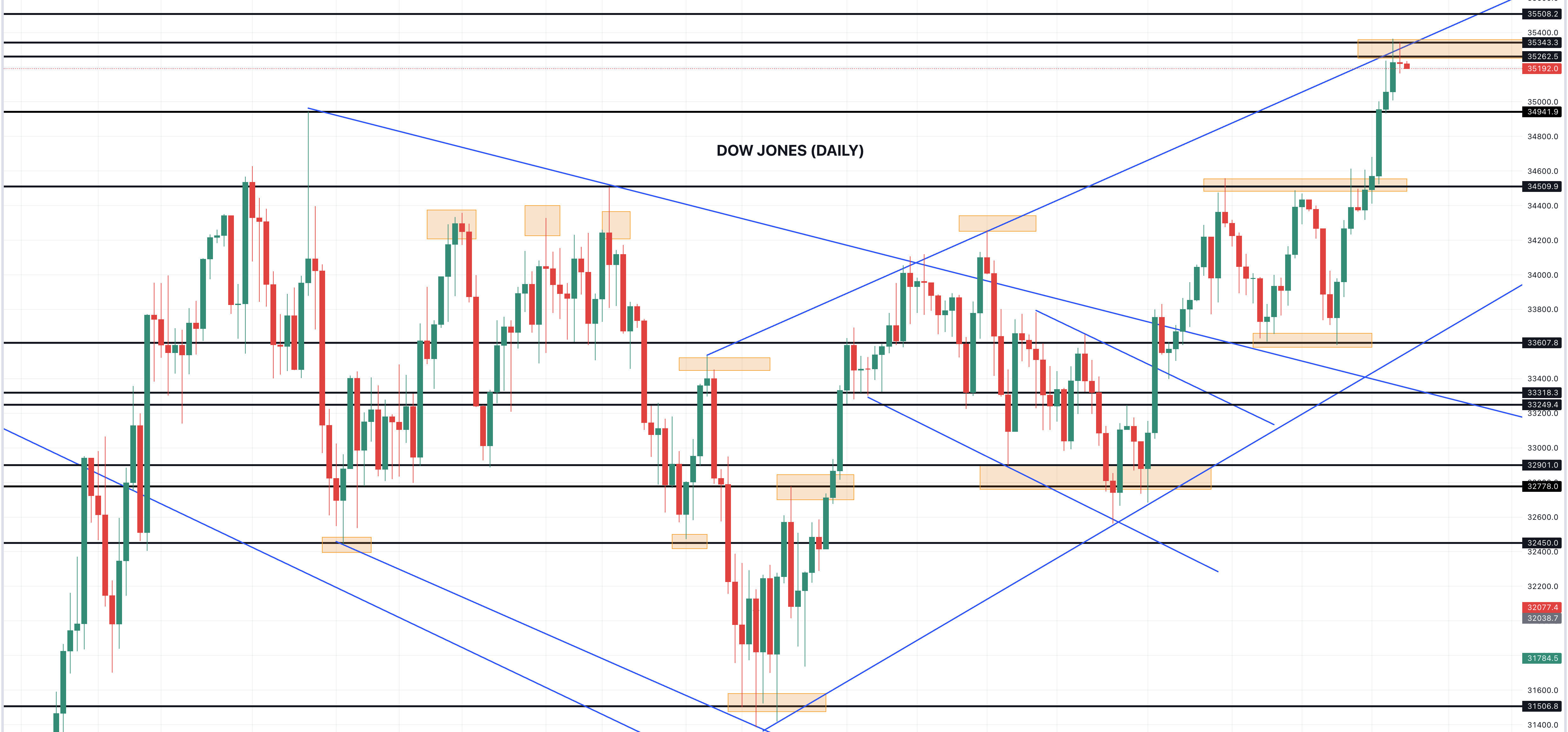

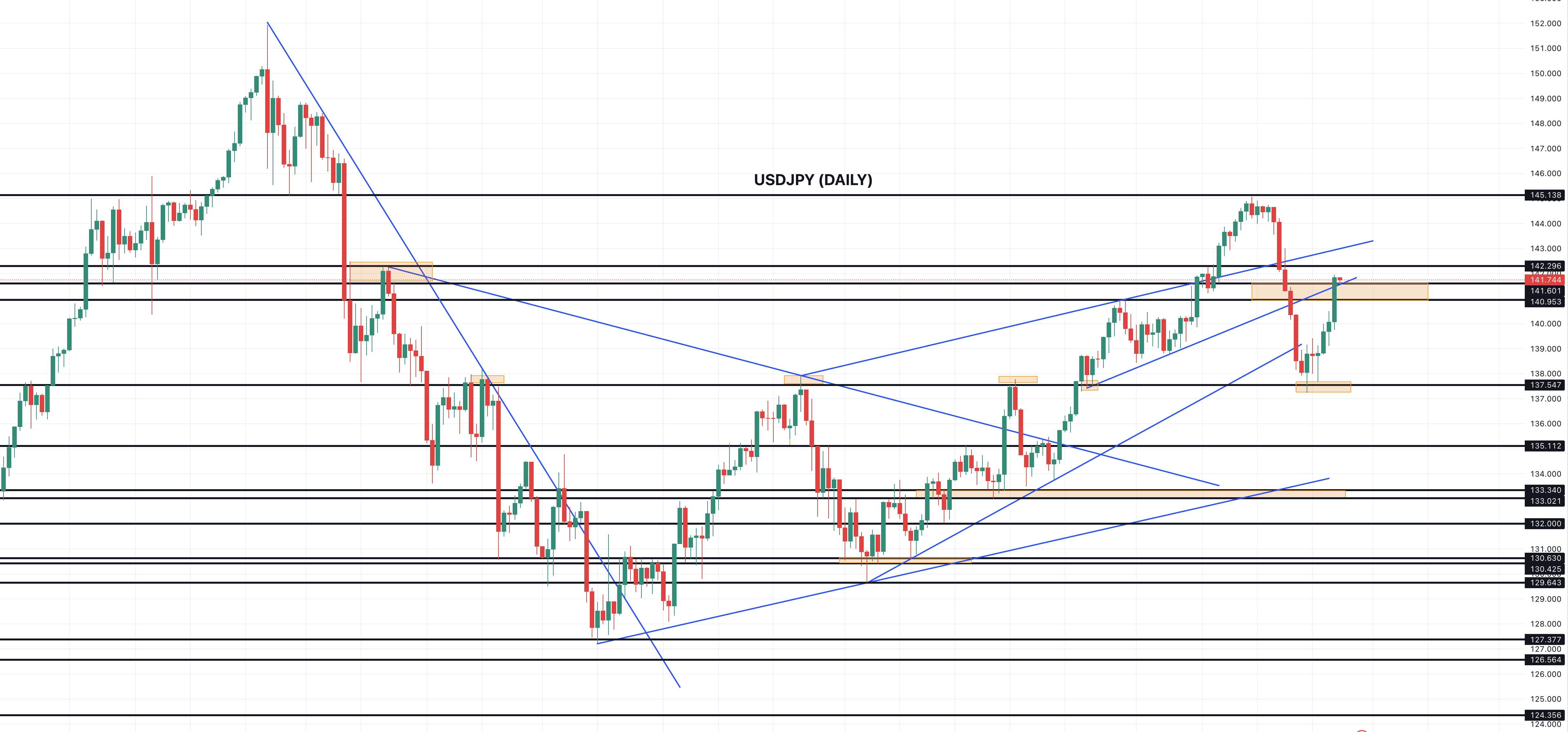

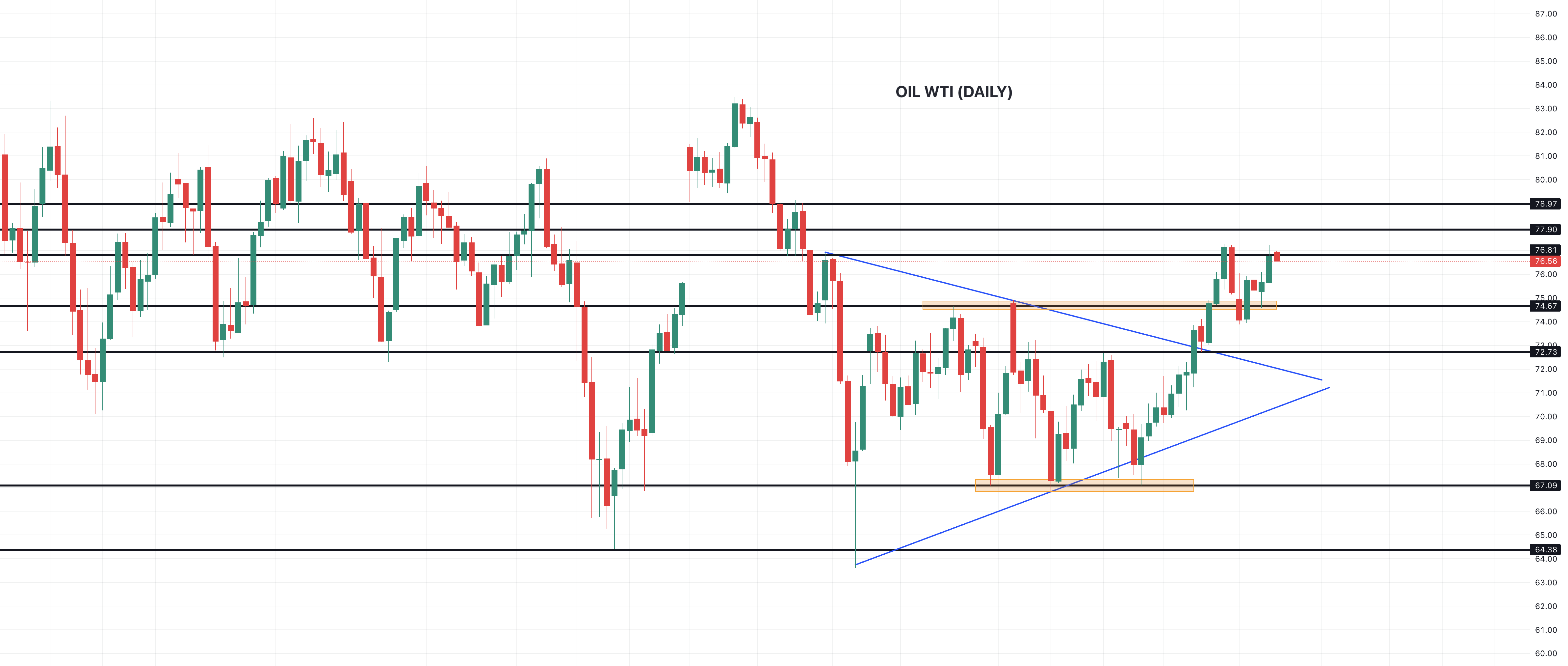

Following another strong week for both U.S. stocks and the Dollar, investors await the upcoming FED rate decision amid a busy week. Stocks have benefited from stronger-than-expected financial results from big names during the beginning of last week which pushed major averages to extend their advance, however, the Nasdaq retreated as some tech-giants companies dragged the index lower. On Friday, we have seen a mixed close as volatility increased due to large stock options expiries.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}