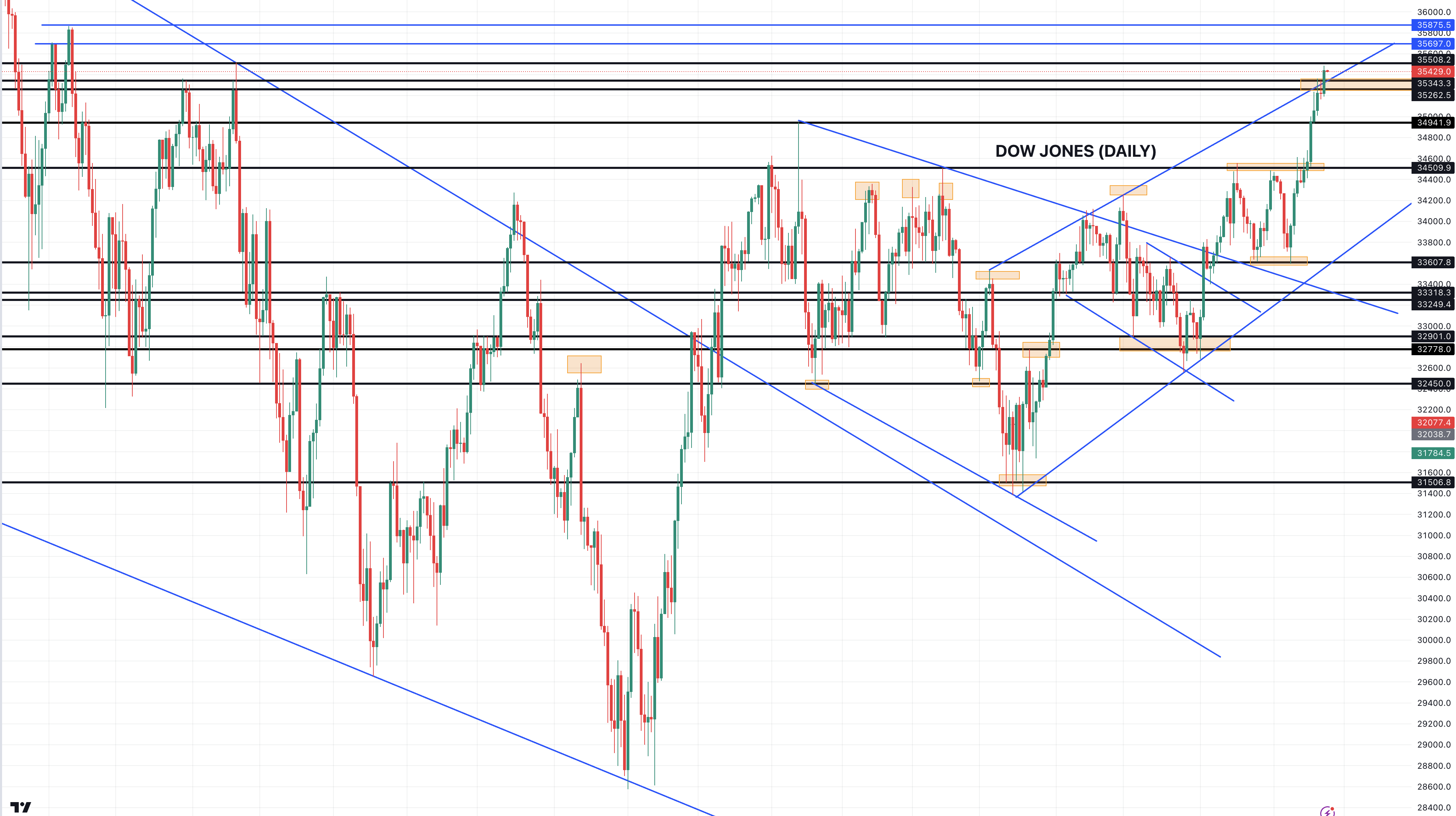

U.S. stocks marked another positive start to the week ahead of the upcoming FED interest rate decision. All major stock market indexes closed higher on Monday with the DOW registering its longest winning streak in six years. The 30-stock index rose for the 11th consecutive day adding 0.52%. In the meantime, the S&P500 climbed 0.40% and the Nasdaq composite gained 0.19% after last week’s decline. Investors also await a set of corporate earnings from big names like Microsoft, Alphabet, and Meta which are due to release their quarterly financial results today and tomorrow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}